python实现马丁策略的实例详解

马丁策略本来是一种赌博方法,但在投资界应用也很广泛,不过对于投资者来说马丁策略过于简单,所以本文将其改进并使得其在震荡市中获利,以下说明如何实现马丁策略。

策略

逢跌加仓,间隔由自己决定,每次加仓是当前仓位的一倍。

连续跌两次卖出,且卖出一半仓位。

如果爆仓则全仓卖出止损。

初始持仓设置为10%~25%,则可进行2到3次补仓。

初始化马丁策略类属性

def __init__(self,startcash, start, end): self.cash = startcash #初始化现金 self.hold = 0 #初始化持仓金额 self.holdper = self.hold /startcash #初始化仓位 self.log = [] #初始化日志 self.cost = 0 #成本价 self.stock_num = 0 #股票数量 self.starttime = start #起始时间 self.endtime = end #终止时间 self.quantlog = [] #交易量记录 self.earn = [] #总资产记录 self.num_log = [] self.droplog = [0]

为了记录每次买卖仓位的变化初始化了各种列表。

交易函数

首先导入需要的模块

import pandas as pd import numpy as np import tushare as ts import matplotlib.pyplot as plt

def buy(self, currentprice, count):

self.cash -= currentprice*count

self.log.append('buy')

self.hold += currentprice*count

self.holdper = self.hold / (self.cash+ self.hold)

self.stock_num += count

self.cost = self.hold / self.stock_num

self.quantlog.append(count//100)

print('买入价:%.2f,手数:%d,现在成本价:%.2f,现在持仓:%.2f,现在筹码:%d' %(currentprice ,count//100, self.cost, self.holdper, self.stock_num//100))

self.earn.append(self.cash+ currentprice*self.stock_num)

self.num_log.append(self.stock_num)

self.droplog = [0]

def sell(self, currentprice, count):

self.cash += currentprice*count

self.stock_num -= count

self.log.append('sell')

self.hold = self.stock_num*self.cost

self.holdper = self.hold / (self.cash + self.hold)

#self.cost = self.hold / self.stock_num

print('卖出价:%.2f,手数:%d,现在成本价:%.2f,现在持仓:%.2f,现在筹码:%d' %(currentprice ,count//100, self.cost, self.holdper, self.stock_num//100))

self.quantlog.append(count//100)

self.earn.append(self.cash+ currentprice*self.stock_num)

self.num_log.append(self.stock_num)

def holdstock(self,currentprice):

self.log.append('hold')

#print('持有,现在仓位为:%.2f。现在成本:%.2f' %(self.holdper,self.cost))

self.quantlog.append(0)

self.earn.append(self.cash+ currentprice*self.stock_num)

self.num_log.append(self.stock_num)

持仓成本的计算方式是利用总持仓金额除以总手数,卖出时不改变持仓成本。持有则是不做任何操作只记录日志

数据接口

def get_stock(self, code): df=ts.get_k_data(code,autype='qfq',start= self.starttime ,end= self.endtime) df.index=pd.to_datetime(df.date) df=df[['open','high','low','close','volume']] return df

数据接口使用tushare,也可使用pro接口,到官网注册领取token。

token = '输入你的token' pro = ts.pro_api() ts.set_token(token) def get_stock_pro(self, code): code = code + '.SH' df = pro.daily(ts_code= code, start_date = self.starttime, end_date= self.endtime) return df

数据结构:

回测函数

def startback(self, data, everyChange, accDropday):

"""

回测函数

"""

for i in range(len(data)):

if i < 1:

continue

if i < accDropday:

drop = backtesting.accumulateVar(everyChange, i, i)

#print('现在累计涨跌幅度为:%.2f'%(drop))

self.martin(data[i], data[i-1], drop, everyChange,i)

elif i < len(data)-2:

drop = backtesting.accumulateVar(everyChange, i, accDropday)

#print('现在累计涨跌幅度为:%.2f'%(drop))

self.martin(data[i],data[i-1], drop, everyChange,i)

else:

if self.stock_num > 0:

self.sell(data[-1],self.stock_num)

else: self.holdstock(data[i])

因为要计算每日涨跌幅,要计算差分,所以第一天的数据不能计算在for循环中跳过,accDropday是累计跌幅的最大计算天数,用来控制入场,当累计跌幅大于某个数值且仓位为0%时可再次入场。以下是入场函数:

def enter(self, currentprice,ex_price,accuDrop):

if accuDrop < -0.01:#and ex_price > currentprice:

count = (self.cash+self.hold) *0.24 // currentprice //100 * 100

print('再次入场')

self.buy(currentprice, count)

else: self.holdstock(currentprice)

入场仓位选择0.24则可进行两次抄底,如果抄底间隔为7%可承受最大跌幅为14%。

策略函数

def martin(self, currentprice, ex_price, accuDrop,everyChange,i):

diff = (ex_price - currentprice)/ex_price

self.droplog.append(diff)

if sum(self.droplog) <= 0:

self.droplog = [0]

if self.stock_num//100 > 1:

if sum(self.droplog) >= 0.04:

if self.holdper*2 < 0.24:

count =(self.cash+self.hold) *(0.25-self.holdper) // currentprice //100 * 100

self.buy(currentprice, count)

elif self.holdper*2 < 1 and (self.hold/currentprice)//100 *100 > 0 and backtesting.computeCon(self.log) < 5:

self.buy(currentprice, (self.hold/currentprice)//100 *100)

else: self.sell(currentprice, self.stock_num//100 *100);print('及时止损')

elif (everyChange[i-2] < 0 and everyChange[i-1] <0 and self.cost < currentprice):# or (everyChange[i-1] < -0.04 and self.cost < currentprice):

if (self.stock_num > 0) and ((self.stock_num*(1/2)//100*100) > 0):

self.sell(currentprice, self.stock_num*(1/2)//100*100 )

#print("现在累计涨跌幅为: %.3f" %(accuDrop))

elif self.stock_num == 100: self.sell(currentprice, 100)

else: self.holdstock(currentprice)

else: self.holdstock(currentprice)

else: self.enter(currentprice,ex_price,accuDrop)

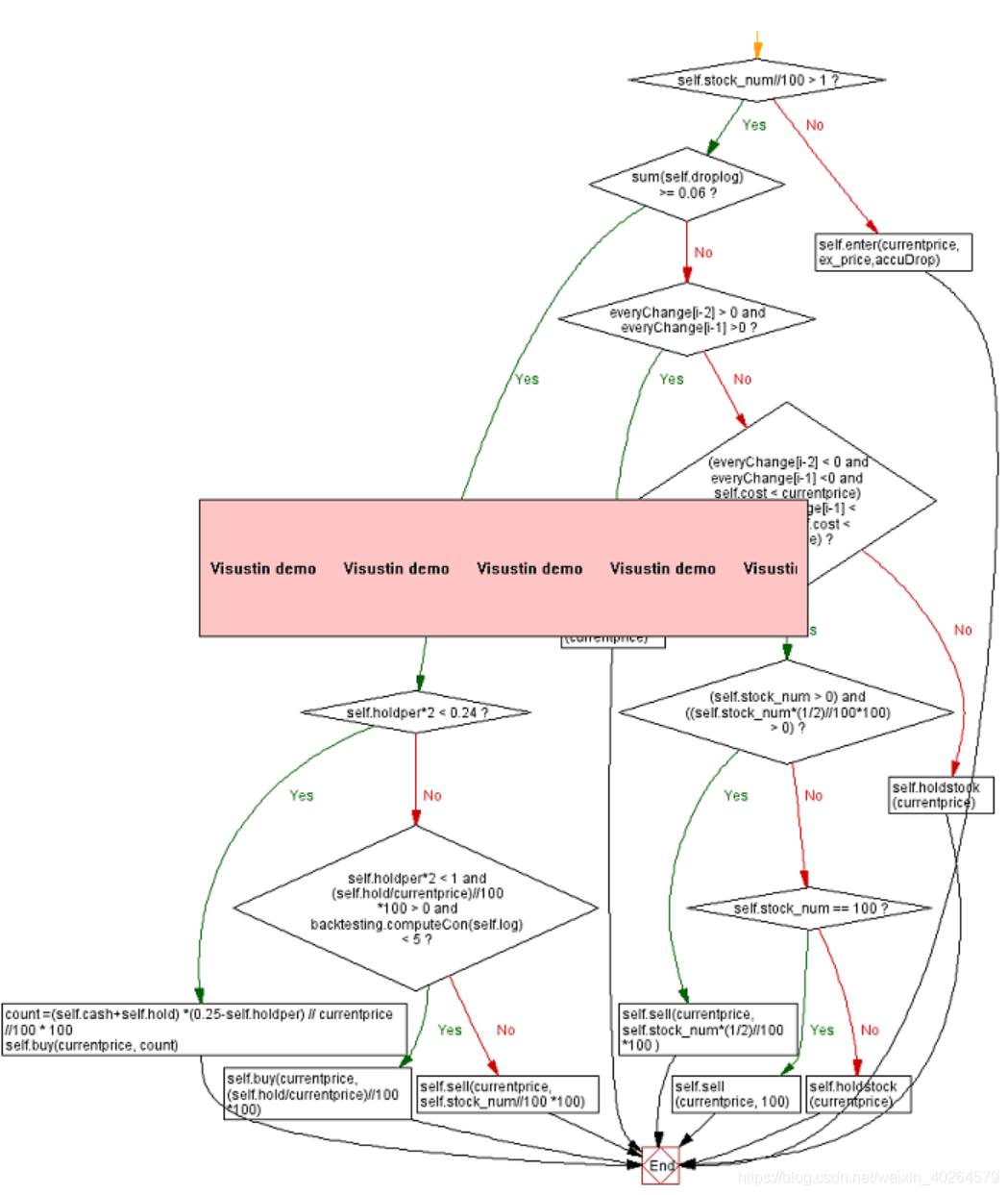

首先构建了droplog专门用于计算累计涨跌幅,当其大于0时重置为0,每次购买后也将其重置为0。当跌幅大于0.04则买入,一下为流程图(因为作图软件Visustin为试用版所以有水印,两个图可以结合来看):

此策略函数可以改成其他策略甚至是反马丁,因为交易函数可以通用。

作图和输出结果

buylog = pd.Series(broker.log)

close = data.copy()

buy = np.zeros(len(close))

sell = np.zeros(len(close))

for i in range(len(buylog)):

if buylog[i] == 'buy':

buy[i] = close[i]

elif buylog[i] == 'sell':

sell[i] = close[i]

buy = pd.Series(buy)

sell = pd.Series(sell)

buy.index = close.index

sell.index = close.index

quantlog = pd.Series(broker.quantlog)

quantlog.index = close.index

earn = pd.Series(broker.earn)

earn.index = close.index

buy = buy.loc[buy > 0]

sell = sell.loc[sell>0]

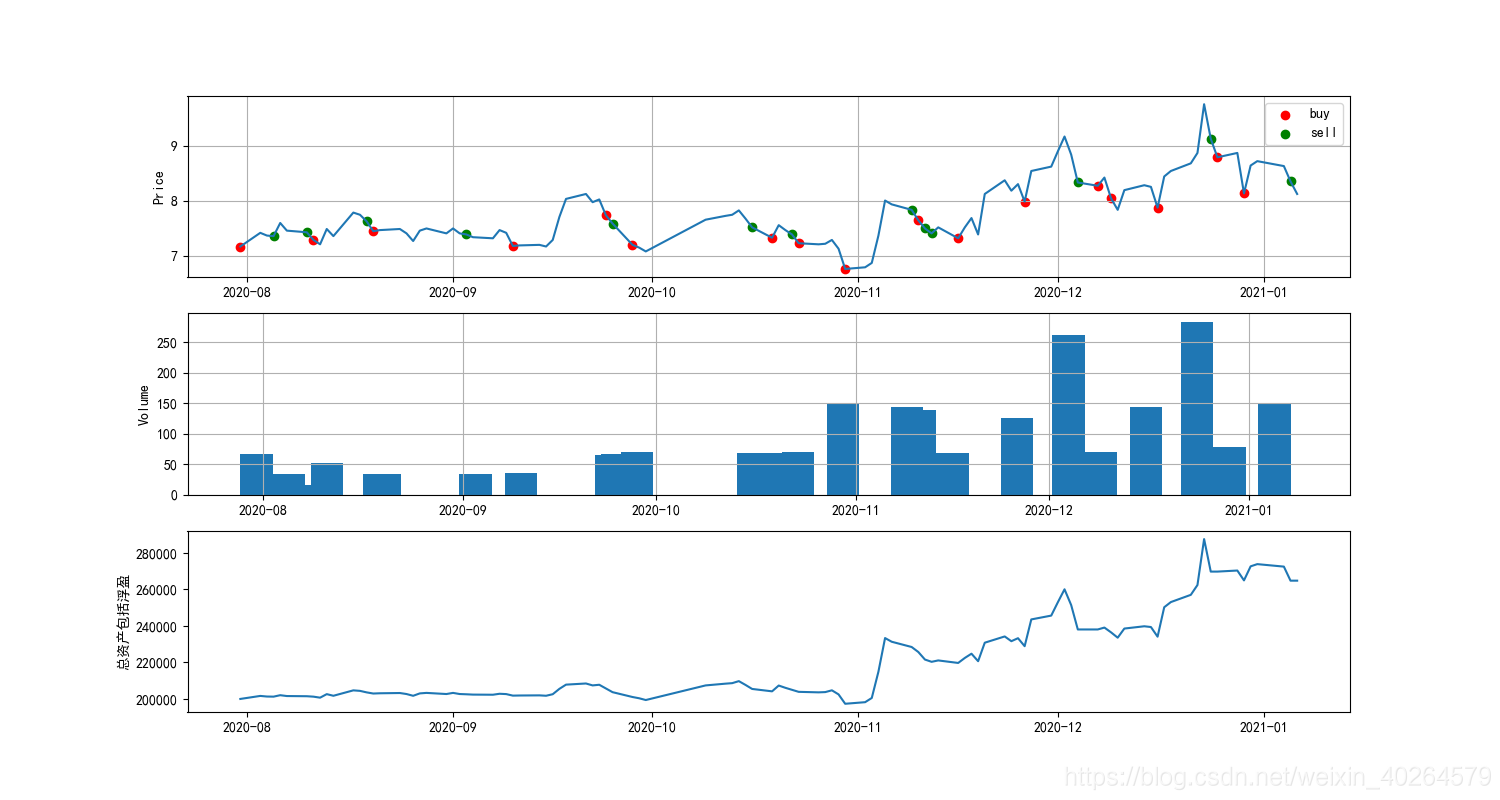

plt.plot(close)

plt.scatter(buy.index,buy,label = 'buy')

plt.scatter(sell.index,sell, label = 'sell')

plt.title('马丁策略')

plt.legend()

#画图

plt.rcParams['font.sans-serif'] = ['SimHei']

fig, (ax1, ax2, ax3) = plt.subplots(3,figsize=(15,8))

ax1.plot(close)

ax1.scatter(buy.index,buy,label = 'buy',color = 'red')

ax1.scatter(sell.index,sell, label = 'sell',color = 'green')

ax1.set_ylabel('Price')

ax1.grid(True)

ax1.legend()

ax1.xaxis_date()

ax2.bar(quantlog.index, quantlog, width = 5)

ax2.set_ylabel('Volume')

ax2.xaxis_date()

ax2.grid(True)

ax3.xaxis_date()

ax3.plot(earn)

ax3.set_ylabel('总资产包括浮盈')

plt.show()

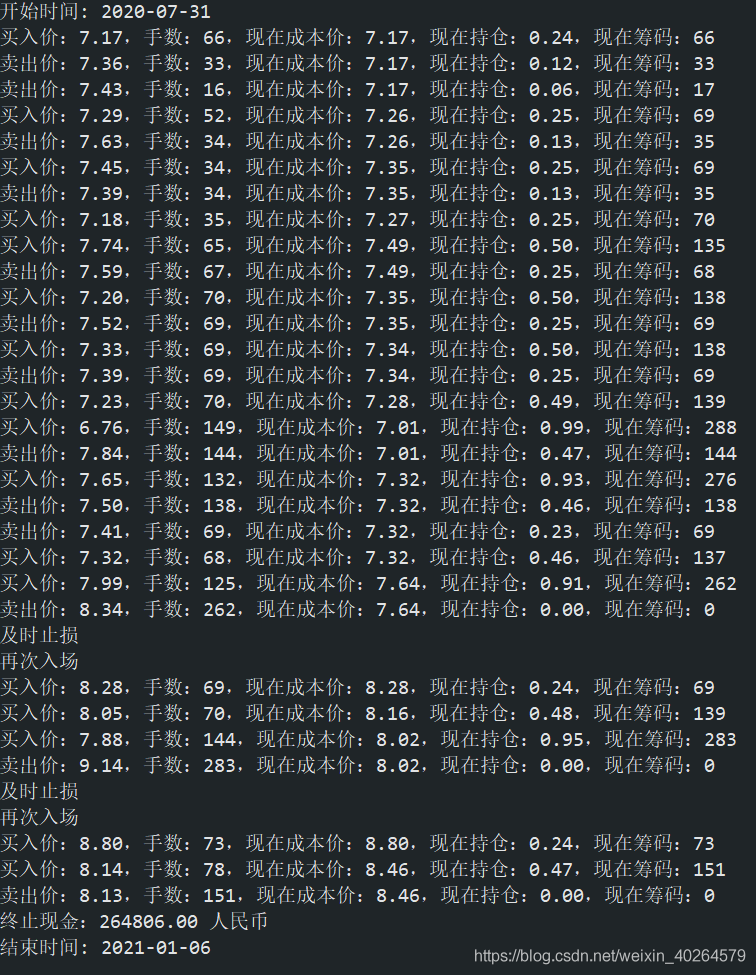

交易日志

到此这篇关于python实现马丁策略的实例详解的文章就介绍到这了,更多相关python马丁策略内容请搜索我们以前的文章或继续浏览下面的相关文章希望大家以后多多支持我们!

相关推荐

-

python解决网站的反爬虫策略总结

本文详细介绍了网站的反爬虫策略,在这里把我写爬虫以来遇到的各种反爬虫策略和应对的方法总结一下. 从功能上来讲,爬虫一般分为数据采集,处理,储存三个部分.这里我们只讨论数据采集部分. 一般网站从三个方面反爬虫:用户请求的Headers,用户行为,网站目录和数据加载方式.前两种比较容易遇到,大多数网站都从这些角度来反爬虫.第三种一些应用ajax的网站会采用,这样增大了爬取的难度(防止静态爬虫使用ajax技术动态加载页面). 1.从用户请求的Headers反爬虫是最常见的反爬虫策略. 伪装header

-

轻松掌握python设计模式之策略模式

本文实例为大家分享了python策略模式代码,供大家参考,具体内容如下 """ 策略模式 """ import types class StrategyExample: def __init__(self, func=None): self.name = '策略例子0' if func is not None: """给实例绑定方法用的,不会影响到其他实例""" self.execute

-

浅谈python量化 双均线策略(金叉死叉)

#小策略,策略逻辑是在金叉时候买进,死叉时候卖出,所谓金叉死叉是两条均线的交叉,当短期均线上穿长期均线为金叉,反之为死叉 #下面是策略代码及结构 # 导入函数库 from jqdata import * # 初始化函数 def initialize(context): # 设定沪深300作为基准 set_benchmark('000300.XSHG') # True为开启动态复权模式,使用真实价格交易 set_option('use_real_price', True) # 股票类交易手续费是:

-

python实现马丁策略的实例详解

马丁策略本来是一种赌博方法,但在投资界应用也很广泛,不过对于投资者来说马丁策略过于简单,所以本文将其改进并使得其在震荡市中获利,以下说明如何实现马丁策略. 策略 逢跌加仓,间隔由自己决定,每次加仓是当前仓位的一倍. 连续跌两次卖出,且卖出一半仓位. 如果爆仓则全仓卖出止损. 初始持仓设置为10%~25%,则可进行2到3次补仓. 初始化马丁策略类属性 def __init__(self,startcash, start, end): self.cash = startcash #初始化现金 sel

-

Python设计模式之策略模式实例详解

本文实例讲述了Python设计模式之策略模式.分享给大家供大家参考,具体如下: 策略模式(Strategy Pattern):它定义了算法家族,分别封装起来,让他们之间可以相互替换,此模式让算法的变化,不会影响到使用算法的客户. 下面是一个商场活动的实现 #!/usr/bin/env python # -*- coding:utf-8 -*- __author__ = 'Andy' ''' 大话设计模式 设计模式--策略模式 策略模式(strategy):它定义了算法家族,分别封装起来,让他们之

-

Python 通过URL打开图片实例详解

Python 通过URL打开图片实例详解 不论是用OpenCV还是PIL,skimage等库,在之前做图像处理的时候,几乎都是读取本地的图片.最近尝试爬虫爬取图片,在保存之前,我希望能先快速浏览一遍图片,然后有选择性的保存.这里就需要从url读取图片了.查了很多资料,发现有这么几种方法,这里做个记录. 本文用到的图片URL如下: img_src = 'http://wx2.sinaimg.cn/mw690/ac38503ely1fesz8m0ov6j20qo140dix.jpg' 1.用Open

-

Python命令启动Web服务器实例详解

Python命令启动Web服务器实例详解 利用Python自带的包可以建立简单的web服务器.在DOS里cd到准备做服务器根目录的路径下,输入命令: python -m Web服务器模块 [端口号,默认8000] 例如: python -m SimpleHTTPServer 8080 然后就可以在浏览器中输入 http://localhost:端口号/路径 来访问服务器资源. 例如: http://localhost:8080/index.htm(当然index.htm文件得自己创建) 其他机器

-

python 二分查找和快速排序实例详解

思想简单,细节颇多:本以为很简单的两个小程序,写起来发现bug频出,留此纪念. #usr/bin/env python def binary_search(lst,t): low=0 height=len(lst)-1 quicksort(lst,0,height) print lst while low<=height: mid = (low+height)/2 if lst[mid] == t: return lst[mid] elif lst[mid]>t: height=mid-1 e

-

Python探索之URL Dispatcher实例详解

URL dispatcher简单点理解就是根据URL,将请求分发到相应的方法中去处理,它是对URL和View的一个映射,它的实现其实也很简单,就是一个正则匹配的过程,事先定义好正则表达式和该正则表达式对应的view方法,如果请求的URL符合这个正则表达式,那么就分发这个请求到这个view方法中. 有了这个base,我们先抛出几个问题,提前思考一下: 这个映射定义在哪里?当映射很多时,如果有效的组织? URL中的参数怎么获取,怎么传给view方法? 如何在view或者是template中反解出UR

-

Python 中迭代器与生成器实例详解

Python 中迭代器与生成器实例详解 本文通过针对不同应用场景及其解决方案的方式,总结了Python中迭代器与生成器的一些相关知识,具体如下: 1.手动遍历迭代器 应用场景:想遍历一个可迭代对象中的所有元素,但是不想用for循环 解决方案:使用next()函数,并捕获StopIteration异常 def manual_iter(): with open('/etc/passwd') as f: try: while True: line=next(f) if line is None: br

-

python 换位密码算法的实例详解

python 换位密码算法的实例详解 一前言: 换位密码基本原理:先把明文按照固定长度进行分组,然后对每一组的字符进行换位操作,从而实现加密.例如,字符串"Error should never pass silently",使用秘钥1432进行加密时,首先将字符串分成若干长度为4的分组,然后对每个分组的字符进行换位,第1个和第3个字符位置不变,把第2个字符和第4个字符交换位置,得到"Eorrrs shluoden v repssa liseltny" 二 代码:

-

Python 高级专用类方法的实例详解

Python 高级专用类方法的实例详解 除了 __getitem__ 和 __setitem__ 之外 Python 还有更多的专用函数.某些可以让你模拟出你甚至可能不知道的功能.下面的例子将展示 UserDict 一些其他专用方法. def __repr__(self): return repr(self.data) (1) def __cmp__(self, dict): (2) if isinstance(dict, UserDict): return cmp(self.data, dic

-

Python 网页解析HTMLParse的实例详解

Python 网页解析HTMLParse的实例详解 使用python将网页抓取下来之后,下一步我们就应该解析网页,提取我们所需要的内容了,在python里提供了一个简单的解析模块HTMLParser类,使用起来也是比较简单的,解析语法没有用到XPath类似的简洁模式,但新手用起来还是比较容易的,看下面的例子: 现在一个模拟的html文件: <html> <title id='main' mouse='你好'>我是标题</title><body>我是内容<